” The answer to this question depends on the legal form of the entity; examples of entity types include sole proprietorships, partnerships, and corporations. A sole proprietorship is a business owned by one person, and its equity would typically consist of a single owner’s capital account. Conversely, a partnership is a business owned by more than one person, with its equity consisting of a separate capital account for each partner.

Accounting Equation Components

All of our content is based on objective analysis, and the opinions are our own. Changes in any one or all of these components will change international student services. The merchandise would decrease by $5,500 and owner’s equity would also decrease by the same amount.

Expanded Accounting Equation Formula

It can be defined as the total number of dollars that a company would have left if it liquidated all of its assets and paid off all of its liabilities. Because of the two-fold effect of business transactions, the equation always stays in balance. Metro Courier, Inc., was organized as a corporation on January 1, the company issued shares (10,000 shares at $3 each) of common stock for $30,000 cash to Ron Chaney, his wife, and their son. Plus, errors are more likely to occur and be missed with single-entry accounting, whereas double-entry accounting provides checks and balances that catch clerical errors and fraud. Almost all businesses use the double-entry accounting system because, truthfully, single-entry is outdated at this point. For example, if a business signs up for accounting software, it will automatically default to double-entry.

Ask Any Financial Question

The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement. The balance sheet is also known as the statement of financial position and it reflects the accounting equation. The balance sheet reports a company’s assets, liabilities, and owner’s (or stockholders’) equity at a specific point in time.

The relationship between the accounting equation and your balance sheet

This long-form equation is called the expanded accounting equation. On the other hand, equity refers to shareholder’s or owner’s equity, which is how much the shareholder or owner has staked into the company. Small business owners typically have a 100% stake in their company, while growing businesses may have an investor and share 20%.

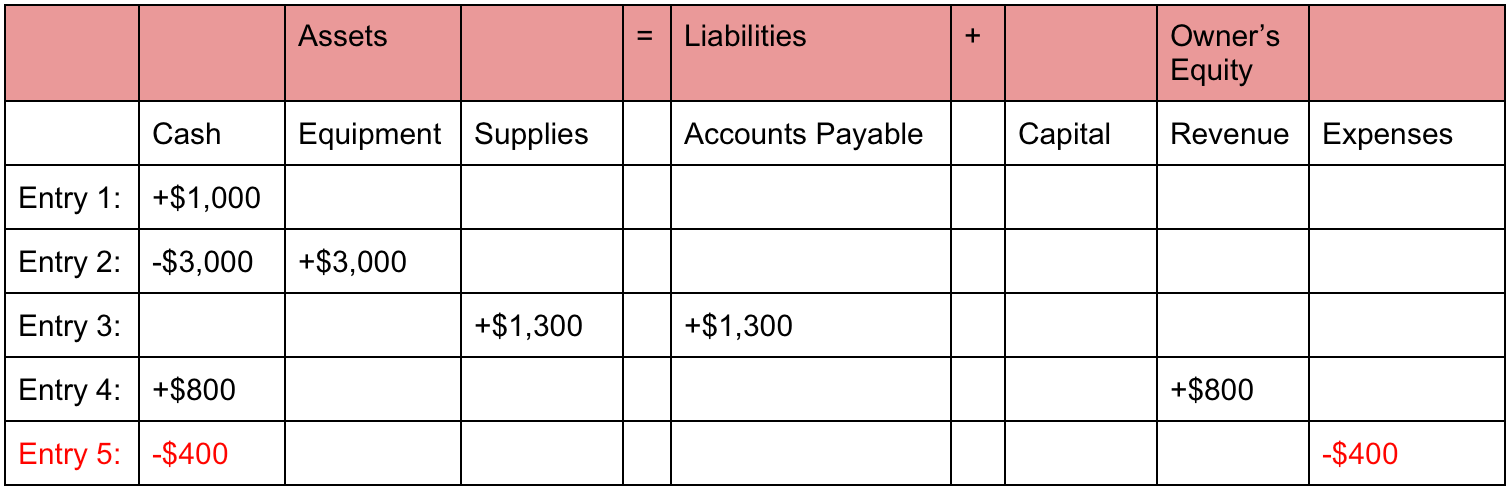

$10,000 of cash (asset) will be received from the bank but the business must also record an equal amount representing the fact that the loan (liability) will eventually need to be repaid. Required Explain how each of the above transactions impact the accounting equation and illustrate the cumulative effect that they have. After the company formation, Speakers, Inc. needs to buy some equipment for installing speakers, so it purchases $20,000 of installation equipment from a manufacturer for cash. In this case, Speakers, Inc. uses its cash to buy another asset, so the asset account is decreased from the disbursement of cash and increased by the addition of installation equipment.

As a result of this transaction, an asset (i.e., cash) increases by $10,000 while another asset ( i.e., merchandise) decreases by $9,000 (the original cost). Capital essentially represents how much the owners have invested into the business along with any accumulated retained profits or losses. The capital would ultimately belong to you as the business owner. Owners can increase their ownership share by contributing money to the company or decrease equity by withdrawing company funds. Likewise, revenues increase equity while expenses decrease equity. A liability, in its simplest terms, is an amount of money owed to another person or organization.

For a company keeping accurate accounts, every business transaction will be represented in at least two of its accounts. For instance, if a business takes a loan from a bank, the borrowed money will be reflected in its balance sheet as both an increase in the company’s assets and an increase in its loan liability. It’s a tool used by company leaders, investors, and analysts that better helps them understand the business’s financial health in terms of its assets versus liabilities and equity. This equation should be supported by the information on a company’s balance sheet. The Accounting Equation is the foundation of double-entry accounting because it displays that all assets are financed by borrowing money or paying with the money of the business’s shareholders. The accounting method under which revenues are recognized on the income statement when they are earned (rather than when the cash is received).

- Corporate shares are easily transferable, with the current holder(s) of the stock being the owners.

- A liability, in its simplest terms, is an amount of money owed to another person or organization.

- The accounting equation plays a significant role as the foundation of the double-entry bookkeeping system.

- Still, you’ll likely see this equation pop up time and time again.

As you can see, all of these transactions always balance out the accounting equation. This equation holds true for all business activities and transactions. If assets increase, either liabilities or owner’s equity must increase to balance out the equation. The equation is generally written with liabilities appearing before owner’s equity because creditors usually have to be repaid before investors in a bankruptcy. In this sense, the liabilities are considered more current than the equity.

Implicit to the notion of a liability is the idea of an “existing” obligation to pay or perform some duty. Liabilities and capital were not affected in transaction #3. Equity represents the portion of company assets that shareholders or partners own. In other words, the shareholders or partners own the remainder of assets once all of the liabilities are paid off. The 500 year-old accounting system where every transaction is recorded into at least two accounts.

This simple formula can also be expressed in three other ways, which we’ll cover next. At first glance, this may look overwhelming — but don’t worry because all three reveal the same information; it just depends on what kind of information you’re looking for. Analyze a company’s financial records as an analyst on a technology team in this free job simulation. Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources.

Leave a Reply